New Zealand’s economic model assumes growth will stabilise the system. But as structural constraints build, that assumption is becoming less reliable. This is not a forecast—it’s a strategy question.

Global fuel disruptions, sudden tariffs and extreme weather events remind us that stability is not a natural equilibrium, but requires coordination.

New Zealand’s economic strategy rests on a historically validated assumption that growth will continue to do the work of maintaining system stability. When the economy expands, households earn and consume more, firms grow profits and governments can invest and redistribute without materially increasing tax burdens. Growth coordinates and aligns conflicting social, capital and fiscal objectives. It softens trade-offs, stabilising the system.

But what if growth becomes less reliable in performing that role? That is the scenario New Zealand is not explicitly planning for.

When Growth Stops Delivering

By international standards, New Zealand has a high-performing economy, ranking among advanced nations on measures of wellbeing and human development.

But GDP growth has slowed in recent years and key wellbeing drivers have weakened:

- Labour is underutilised. Unemployment and underutilisation are rising, indicating that many people want to work more.

- Living standards are under pressure. Purchasing power has stagnated in many households. Cost pressures in housing, food and energy remain elevated.

- Small business performance has softened. Profitability and survival rates lag historical norms.

- Fiscal headroom has narrowed. Consolidation efforts are ongoing but the outlook has switched from stable to negative.

- Infrastructure gaps are visible. Transport, water and housing systems face persistent underinvestment.

- Retirement protections are under strain. Superannuation provides stability but is becoming more costly, while private retirement outcomes are more volatile and unequal.

Individually, many of these issues are manageable. Collectively, they suggest economic dependence on growth: when growth slows, multiple system outcomes deteriorate simultaneously.

A straightforward response is to restore stronger growth. But that’s not so easy.

Why Growth Is Becoming Less Reliable

Economic slowdowns are not new. Historically, cyclical shocks have been absorbed through macroeconomic policy, with growth eventually recovering.

The greater challenge lies in structural constraints that may reduce the ceiling of growth over time.

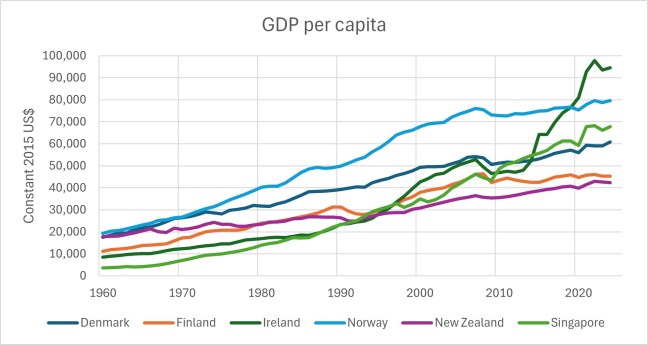

Relative to comparable small advanced economies (e.g. Nordic countries, Ireland and Singapore), New Zealand’s GDP per capita has grown more slowly over recent decades and appears to be levelling off (see figure 1). This suggests persistent structural weakness rather than episodic shocks.

Figure 1: GDP per capita 1960-2024 for small advanced economies. World Bank data retrieved here.

Key constraints include:

- A productivity challenge. Growth has relied more on labour expansion than productivity gains. Sectoral concentration in agriculture, tourism and low-scale services limits movement into higher-value, knowledge-intensive industries.

- Shifting income distribution. The labour share of income has declined over time. Domestic demand has become more reliant on credit expansion, asset inflation and fiscal support, increasing financial vulnerability.

- Capital allocation bias. Limited domestic investment opportunities have channelled capital into housing and financial assets, constraining productivity-enhancing investment.

- Demographic headwinds. Population ageing increases fiscal pressure while reducing labour force growth.

- Structural smallness and distance. A small domestic market and geographic isolation limit scale, competition and diversification.

- Environmental limits. Land, water and emissions limits are increasingly binding, with climate impacts raising the cost of maintaining infrastructure and assets.

New Zealand’s Paradox: Strong Outcomes, Emerging Constraints

New Zealand presents an apparent contradiction. Despite slower GDP per capita growth, it continues to deliver relatively high levels of wellbeing, though recent trends show deterioration.

This reflects accumulated advantages: strong public institutions, abundant natural resources, social cohesion and legacy investments in infrastructure and the welfare system. These have supported outcomes even as growth has moderated.

However, forward pressures are intensifying:

- Ageing population: rising pension and healthcare costs

- Climate adaptation: higher capital maintenance burden

- Infrastructure deficits: large, ongoing investment needs

- Environmental constraints: limits to primary sector expansion

A credible counterview is that these constraints are not binding, but reflect policy choices. Structural reform, deeper capital markets and technological change could lift productivity and restore stronger growth trajectories, as seen in other small advanced economies.

But the effects of these measures are uncertain, uneven and may introduce new trade-offs. Even with improved policy settings, structural features such as scale, distance, demographics and environmental limits are likely to persist.

The issue is not whether the upside case for growth is possible. It is whether it is sufficiently reliable to anchor system stability.

This is not a forecasting debate about whether growth will occur. It is a strategy question: should system stability depend on growth if its reliability is uncertain?

The Strategic Risk: When Growth No Longer Stabilises

Modern economic systems are designed to maintain stability across three domains:

- Macroeconomic stability (employment, inflation, fiscal balance).

- Social stability (living standards, distribution, political legitimacy).

- Structural stability (functional resilience under changing conditions).

Growth has historically stabilised these by easing trade-offs. When growth slows down, those trade-offs re-emerge.

- Redistribution competes with fiscal sustainability.

- Affordability compresses business margins.

- Environmental limits constrain expansion.

- Wage growth conflicts with employment.

- Global efficiency reduces domestic resilience.

Sustained low growth makes these tensions more explicit and politically salient.

New Zealand has so far avoided the deeper polarisation seen elsewhere, buffered by institutional trust and social cohesion, including Māori tikanga. However, pressures are mounting, including housing inequality, intergenerational divides and distributional tensions.

If expectations continue to outpace outcomes, the economic risk is erosion of system legitimacy.

Reframing The Objective: From Growth To Stability

The core strategic question is not how to sustain growth, but how to sustain economic and social stability under conditions where growth may be weak, uneven or constrained.

This reframing shifts growth from being the objective of the system to one of several possible outcomes. When growth contributes to wellbeing, it is beneficial. But it is no longer relied upon as the sole stabilising mechanism.

This distinction is material. When growth is treated as a goal, policy and business strategy tend to prioritise expansion, even when it exacerbates underlying constraints. When stability becomes the goal, the focus shifts to institutional arrangements that deliver secure livelihoods, functional markets and fiscal sustainability across a range of growth outcomes.

The Missing Scenario: Post-Growth As Risk Management

Post-growth can be understood as a system design framework for advanced economies facing structural limits to expansion. It is a risk management approach to ensure system stability if growth is weaker than expected.

It expands the range of plausible futures and reduces exposure to a single point of failure: reliance on growth as the primary stabiliser.

What Changes Under a Post-Growth Scenario

Economic goals remain familiar: secure livelihoods, stable public finances and social legitimacy. What changes is how they are achieved. Stability is designed into institutional functionality rather than emerging from expansion.

- Investment shifts from expansion to maintenance, resilience and public value.

- Productivity gains are translated into reduced working time or improved services.

- Demand is stabilised, reducing reliance on credit expansion.

- Financial systems adapt to lower and more stable returns.

- Employment is distributed differently through work-sharing, sectoral diversification and public employment buffers.

These mechanisms involve trade-offs, including potential efficiency losses. But their role is to stabilise employment and incomes where market-led growth is insufficient.

Table 1 expands the post-growth model across numerous dimensions and compares it with the growth model.

Table 1: A comparison of growth and post-growth models across multiple dimensions.

| Dimension | Growth Economy | Post-Growth Economy |

|---|---|---|

| Core Objective | Maximise GDP growth as the primary means to deliver prosperity and stability | Deliver wellbeing, stability and legitimacy with or without growth |

| Stabilising Logic | Growth aligns competing demands (investment, redistribution, profits) and avoids trade-offs | Institutional design stabilises the system through sufficiency and resilience |

| Risk Assumption | Growth is resilient over the long term | Growth may be persistently weak, uneven or insufficient |

| Strategic Risk | Shocks and cyclical downturns | Structural stagnation undermining fiscal, social and political stability |

| Planning Approach | Scenario planning based on growth cycles: high/low/recession | Adds a fourth scenario: economic and social system stability across a range of growth outcomes |

| Policy Orientation | Stimulate and sustain growth through coordinated macroeconomic and structural policy | Redesign institutions to function under low, uneven or constrained growth |

| Investment | Capital accumulation to expand productive capacity and output | Invest in maintenance, sufficiency, resilience and public goods |

| Productivity | Drives output expansion and income growth | Translated into reduced working time and efficiency gains |

| Resource use and natural capital | Nature inputs are managed via pricing, substitution and technology | Prioritises sufficiency, circularity and regeneration to reduce throughput and preserve natural assets |

| Climate and environment | Manages impacts through efficiency and decoupling; outcomes depend on growth dynamics | Treats ecological limits as binding; prioritises absolute reductions and operating within boundaries |

| Consumer Demand | Expansion of consumption via credit, housing finance and pro-consumption tax settings | Stabilised at sufficiency levels, reducing dependence on continuous demand growth |

| Financial System | Expanding credit and capital markets based on future growth expectations | Growth-agnostic finance: patient capital, stability-oriented lending |

| Labour Markets | Expansion through population growth, immigration and labour activation | Work-sharing, labour time reduction, diversified livelihoods, employment guarantees |

| Competition & Markets | Market competition drives efficiency, innovation and scale | Markets operate alongside government and community in provisioning systems |

| Global Trade | Globalisation enables specialisation, scale and efficiency | Regionalisation and resilience: shorter supply chains, strategic trade dependencies |

| Infrastructure | Expansion of transport, logistics and digital systems to enable growth | Investment in maintenance, adaptation and resilience |

| Innovation | Oriented toward scale, new markets and product turnover | Directed toward mission-oriented outcomes: sustainability, care, durability, circularity |

| Fiscal Model | Relies on expanding tax base from growth to fund services and redistribution | Restructured public finance: stable tax bases, prioritised spending, new fiscal tools |

| Social Contract | Rising incomes and consumption underpin legitimacy | Secure livelihoods, universal basic services and income floors underpin legitimacy |

Implications For New Zealand Policy

New Zealand is not facing imminent economic breakdown, but it is operating with a model under increasing strain. Strategies that rely on restoring higher growth rates face intensifying trade-offs if growth remains constrained.

A post-growth framing does not reject growth as an outcome. It removes reliance on it by building institutions that can manage trade-offs directly.

New Zealand already has elements of this approach:

- A strong public sector.

- Wellbeing-oriented policy frameworks.

- Māori models grounded in stewardship and long-term horizons.

- Increasing focus on resilience and adaptation.

The opportunity is to integrate these into a coherent model.

Implications For Business

For business, post-growth is not a prediction but a strategic scenario.

Firms increasingly plan for multiple futures. Post-growth adds conditions where expansion is constrained or destabilising.

This implies:

- Stress-testing strategies under sustained low-growth assumptions.

- Shifting value creation models from volume to durability and service.

- Investing in resilience across supply chains and workforce.

- Preparing for tighter constraints and regulation.

Competitive advantage shifts toward robustness, not scale alone.

Plan Beyond Growth

For leaders, the task is not to optimise for a particular growth trajectory. It is to ensure stability across a range of growth outcomes. This requires managing trade-offs explicitly: between distribution and investment, efficiency and resilience, consumption and sustainability.

New Zealand has the institutional capability to do this. The risk is discovering too late that growth can no longer carry the system. The opportunity is to ensure that it no longer has to.

Featured image by Simon Berger on Unsplash.